When enrolling at a private school such as Georgetown, there are often “hidden costs” that not all students and their families may be aware of. These costs have the most serious consequences for students from low-income backgrounds and are significant. At Georgetown, the forefront of these hidden costs is the student health insurance policy.

When enrolling at a private school such as Georgetown, there are often “hidden costs” that not all students and their families may be aware of. These costs have the most serious consequences for students from low-income backgrounds and are significant. At Georgetown, the forefront of these hidden costs is the student health insurance policy.

Beginning in 2014, 28 states and the District of Columbia expanded Medicaid eligibility to include households whose income was at least 138% of the federal poverty level. Figures vary according to state, it is currently 210% in D.C. This expansion finally made healthcare accessible to millions of Americans who were previously uninsured.

I applied for and received my first health insurance policy through Medi-Cal, Medicaid of California, earlier this year. When I finally received my card from Anthem Blue Cross, it was the first day of my life that I knew if I fell and broke a bone, it wouldn’t break the bank.

The fear that comes with living uninsured is a feeling known all too well for millions of Americans. For uninsured families, sickness means long waits at free clinics and the overarching fear of the financial strife, or even bankruptcy, that a medical condition could cause. We grow up knowing that the best thing to do when you are sick is to simply hope it passes without escalating. “Unless you’re dying, just wait it out,” was a common phrase in my household growing up.

But all that is supposed to change in college. We have a student health center on campus, a program for student health insurance and a hospital. Certainly it is important when students are living in such close quarters to be able to access adequate health services, if at the very least to prevent the spread of potentially hazardous infectious disease. This is ostensibly why most colleges, including Georgetown, require all students to have full healthcare coverage before enrolling and living on campus.

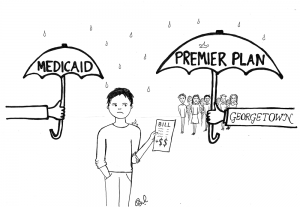

Many Georgetown students have a form of health insurance, either through a private provider or their parents’ job, and are therefore able to waive the Premier Plan. However, for students who are either uninsured or beneficiaries of Medicaid, that is sadly not an option. The Office of Student Health Insurance capitulates the requirements that an existing policy must have in order to waive the Premier Plan — and no out-of-state Medicaid coverage is eligible. This begs an important question: If students who have other health coverage can opt out of it easily, for whom is the Premier Plan designed? It seems likely that it is targeted at low-income students who are otherwise uninsured and cannot afford its high price.

When I received my first Georgetown bill in August, I was surprised to see the $2,375 health insurance fee, a fee that I had not been made aware of earlier during the financial aid process. I called the Office of Student Health Insurance and explained to them that I was receiving state benefits and could not pay for the student coverage. They informed me that my Medi-Cal was not adequate. When I asked if D.C. Medicaid would be accepted, I was told that no information about anything besides the Premier Plan could be provided. Another student was told that she “shouldn’t have come here if she couldn’t afford the Premier Plan.”

As previously mentioned, the expansion of Medicaid in D.C. allows all adults who make less than 210 percent of the federal poverty line to obtain free health care coverage (319 percent for children under the age of 18 and pregnant women, and 216 percent for parents). However, D.C. residency is required — something that a student living in California before Georgetown cannot possibly have. Even if D.C. Medicaid were to be accepted as a viable way to waive the egregious Premier Plan requirement, students wouldn’t be able to obtain coverage until their second year.

Admittedly, the Georgetown endowment is comparatively small, so there is not as much money to devote to student needs, but not small enough that it cannot afford to give low-income students equal access to affordable health coverage. The administration should embody its own values of “women and men for others” and realize that the student health insurance policy is unjust. For Georgetown, University $2,375 might be negligible, but for many low-income students it poses a significant hardship that may prevent them from attending this university, accessing its resources and benefitting from the excellent opportunities that a Georgetown education undoubtedly provides.

I propose that for the first year, Georgetown should waive the cost of the student health insurance plan for families who are beneficiaries of Medicaid or who are uninsured in states that have not expanded Medicaid but whose income falls within federal Medicaid guidelines. After that, the Premier Plan could be waived for D.C. Medicaid. Alternatively, scholarships and/or grants should be available to cover this hidden cost that disproportionately affects low-income students. And last but not least Georgetown should offer counseling and information to its students on different health care options including applications for D.C. Medicaid.

Serafina Smith is a junior in the College.